Like every other aspect of running a business, the accounts payable system is subject to some degree of risk associated with it. Indeed, business-to-business (B2B) transactions that are deceitful or completely unnecessary can result from unknown financial territory, defective records, or other types of anomalies of a similar nature. It is common knowledge that making fraudulent or needless business-to-business payments can have a detrimental effect on a company’s finances, which can sometimes be quite severe.

There will always be some degree of risk associated with running a business. While this is a reality that we have no choice but to accept, some metrics can be utilized to reduce the extent of this risk.

One of these metrics that you may utilize to maintain the safety and security of your company is the accounts payable risk and control matrix. But what are accounts payable risk and control matrix, and how can it help your business? Let’s find out.

What is a payable risk and control matrix?

The accounts payable risk and control matrix is a tool utilized to help businesses reduce the amount of risk they are exposed to as a direct result of their account payables. While it is recommended that organizations be flexible and responsive to changing conditions, it is also a good idea for them to have some sort of risk control matrix. An AP risk and control matrix lays out the many control objectives that must be taken into consideration by businesses. If these controls are not checked regularly, there is a possibility that the company’s risk protection controls will become compromised.

Why your business needs accounts payable risk and control matrix

As a business owner, if your business still lacks an accounts payable risk and control matrix, you might be wondering if it’s really necessary. But the truth of the matter is that this tool is very crucial. Here are some of the reasons why your business needs it:

- Protect against the inherent risks in accounts payable

Processing a significant number of invoices is a consistent requirement for businesses. The accounts payable departments receive many invoices daily, which they must compare to the corresponding purchase orders and pay. There are various ways in which this process might go awry, particularly when your accounting is done manually. This is the kind of labor that carries with it a certain amount of natural danger.

Investopedia describes inherent risk as “the likelihood of erroneous or misleading information in accounting statements originating from something other than the failure of controls.” In other words, inherent risk is not caused by a failure of controls.

Fundamentally, inherent risk results from either a lack of knowledge or errors brought on by unexpected or complicated computations. Thankfully, accounts payable risks and a control matrix can help protect your business from such inherent risks.

- Control prevalence of residual risks

Even when corporations exercise a reasonable amount of prudence and perform rigorous accounting, there is still a possibility of risk. This type of risk is referred to as residual risk, and Compliance Week defines it as “the exposure that remains after you’ve examined the existing controls.”

Residual risk is a type of risk that arises when a company has taken some steps to handle a potential problem but, in one way or another, hasn’t dealt with the issue completely. Residual risk is also referred to as audit risk. It’s the same as when a firm replaces the servers for its internal accounting network but fails to invest in off-site data backups in case of a natural disaster. In that case, the company risks losing all of its financial data.

In addition, negligence is not a necessary condition for there to be a residual risk. Some risks, like inherent risks will likely continue to exist no matter what a corporation does or does not do. Accepting a certain level of risk is one of the ways to run a successful business.

The important thing is to cut down on any inherent or residual risks as much as possible. A risk and control matrix for accounts payable is an excellent tool for accomplishing this goal.

How to build your accounts payable risk and control matrix

Now that you understand what an accounts payable risk and control matrix is and why your business needs it let’s see how you can create matrices to curb the risks mentioned above.

Creating an inherent risk matrix

Because the level of residual risk is decided by the level of inherent risk that has been tabulated, it makes perfect sense to calculate the level of inherent risk before attempting to grasp the concept of residual risk.

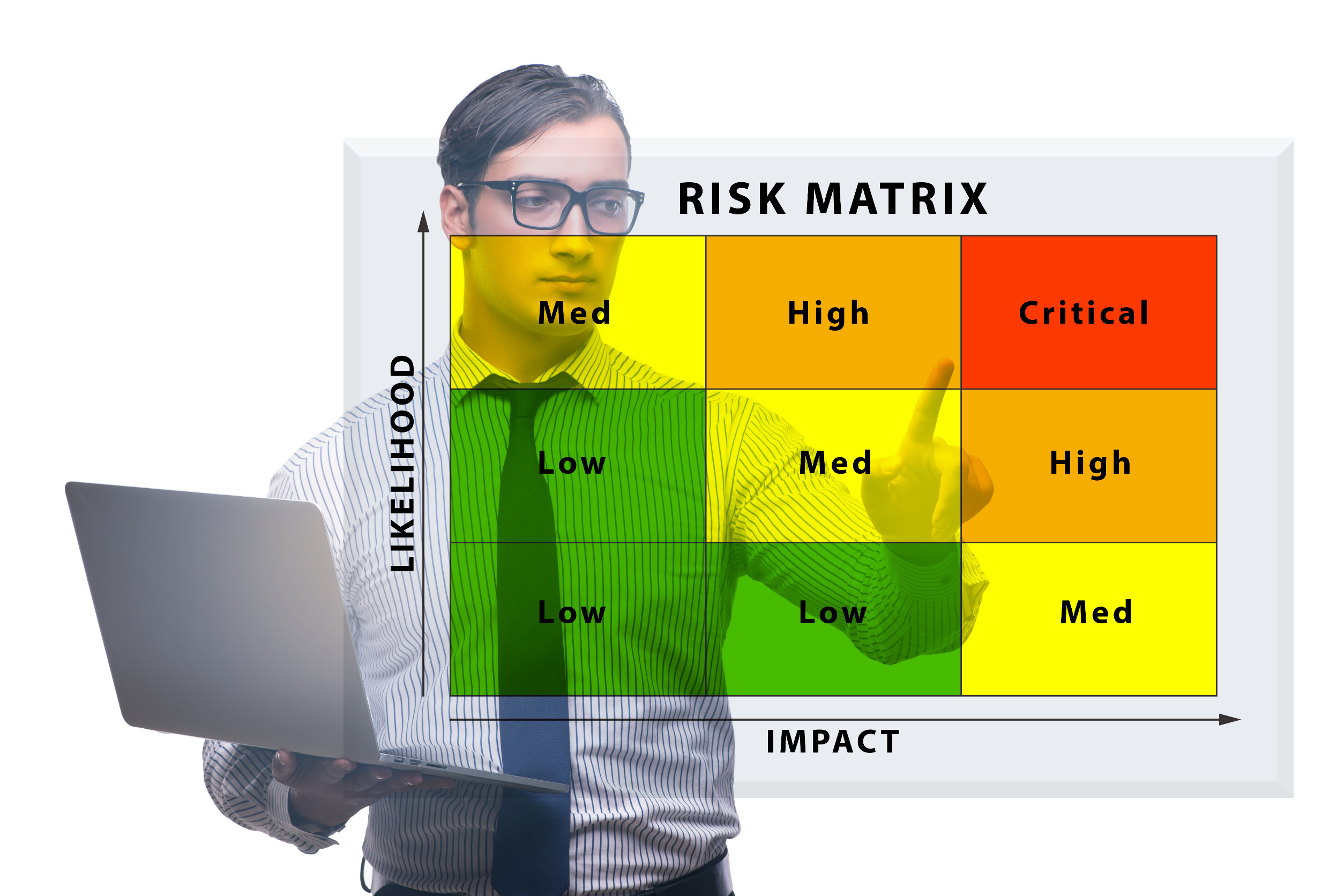

An inherent risk matrix takes a form of a chart. Use a scale that measures potential hazards’ impact on the X-axis. The least risky options should be at the beginning of the axis, and the riskier options should be further along the axis.

For the Y-axis, the scale must indicate the frequency with which the risk occurs, beginning with “Rare” and progressing to increasingly frequent occurrences as the chart continues.

Creating a residual risk matrix

After creating an inherent risk matrix, it is possible to use it to generate a residual risk matrix. Place a scale proportional to the estimated effectiveness of whatever control mechanism your team has designed somewhere along the Y-axis. The scale should begin with a strong value at the bottom and progressively weaken as the Y-axis moves higher. Create, along the X-axis, a scale that ranges from the smallest possible to the largest possible calculated inherent risk.

A residual risk matrix does not need a predetermined number of squares, just like an inherent risk matrix does not have a predetermined number of squares. For consistency and comparability, it is wise to utilize the same number of squares in a residual risk matrix as whatever you’ve selected with your inherent risk matrix. Using the same number of squares in both matrices will ensure that your results are comparable.